As a firm working across multiple sectors, it’s important for us to keep an eye on the various factors affecting the industries in which our clients operate. Spotting trends and potential opportunities is a key part of what we do in order that we can get ahead of the masses in presenting our clients’ investment proposition.

Semiconductors have been a major talking point now for a while and this relatively obscure sector continues to be put under pressure by geopolitical forces. The initial problems started back in 2020 during the COVID19 crisis with cancellations of orders, trade disruption coupled with a spike in demand driven by a sudden shift in working practices from in-person to remote meetings & work. This led to a huge increase in use of items of related equipment such as 5G devices, laptops and wireless communications tech.

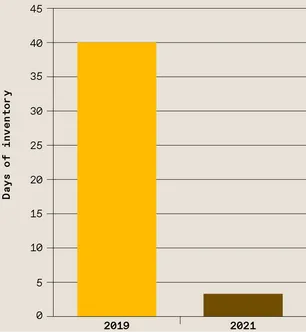

The issues with inventory are appropriately demonstrated by the chart on the left which shows the precipitous decline in global semiconductor inventory between 2019 and 2021 (Source: SIA)

Due to its strengths in fabrication, assembly, and research, China has grown in importance within the global semiconductor industry. One important element is the rapid growth of “fabs”, or semiconductor fabrication facilities. The country has invested heavily in building advanced fabs to manufacture chips at various process nodes.

These fabs enable China to enhance its domestic production capacity, reduce its reliance on foreign semiconductor suppliers, and meet the growing demand for semiconductors within its borders. China has established itself as a key player in the global semiconductor supply chain due to its capacity to manufacture a wide variety of chips, including those used in smartphones, consumer electronics, and industrial applications.

China is a dominant player in the materials industry, particularly in the production of basic materials required for semiconductors. The country’s significance lies both in its abundant reserves of essential materials like silicon but also in its control over critical minerals used in semiconductor production. China holds a significant share of global reserves for critical minerals such as rare earth elements (REE’s), which are vital for manufacturing high-performance semiconductors, magnets, and other advanced technologies.

Its strong position in the critical minerals market affords China substantial influence over the global semiconductor industry. Furthermore, China has implemented strategies to secure a steady supply of these critical minerals, both via domestic production and overseas investments in mining operations. This dominance in critical minerals solidifies China’s role as a critical participant in the global semiconductor supply chain. Western economies are now working hard to reduce reliance on China at the various points in the supply chain.

Now, in the middle of 2023, semiconductors again found their way into the news; at least for those who were paying attention! In October 2022, the Biden led US Administration imposed a number of export controls on US origin semi-conducter equipment and components. Businesses and individuals in China are now, as a result unable to buy advanced chips and chip-making technology from US suppliers without the seller being granted a specific licence from the US government. This was followed by the Netherlands imposing export controls on manufacturing equipment in June 20223. China responded by placing export controls on 2 critical elements; gallium and germanium.

Clearly, the semiconductor industry will continue to be a geopolitical football for quite some time.

We are interested in speaking with any company involved in the semiconductor industry, at any part of the industry vertical.